Introduction

Three major coinsurance transactions — totaling $9.7 billion in standalone LTC reserves — closed between February 2024 and July 2025. After years of near-dormancy, the long-term care (LTC) reinsurance market is active again, drawing in asset managers, private equity firms, and specialist reinsurers who see a repeatable deal structure worth pursuing.

Legacy LTC blocks have long strained insurer capital. Reserve strengthening, a decade of premium rate increases, and a higher interest-rate environment have finally converged to close the pricing gap that kept buyers and sellers apart. Carriers that once viewed their LTC exposure as untradeable are now finding willing counterparties.

This article breaks down what LTC reinsurance is, why the market revived, what drives deal viability, how transactions are structured, and what to expect heading into 2026 and 2027.

Key Takeaways

- Dealer-owned reinsurance allows auto dealers to capture underwriting profits from VSCs, GAP, and ancillary F&I products instead of paying third-party providers

- Admin obligor reinsurance structures are backed by A-rated insurers, giving dealers profit participation without direct insurance liability exposure

- Block performance hinges on product mix, claims experience, premium volume, and how well the dealer's F&I team presents and sells covered products

- DealerRE has helped more than 400 dealers nationwide establish and manage their own reinsurance programs since 1994

- 2025 presents a strong opportunity for dealers to review F&I structures and redirect underwriting profit back into their own reinsurance companies

What Is LTC Reinsurance?

Long-Term Care Insurance Defined

Long-term care insurance covers services that standard health insurance does not: nursing home care, assisted living, and in-home care for individuals who can no longer perform basic daily activities independently. The NAIC Model Act #640 defines it as coverage providing "diagnostic, preventive, therapeutic, rehabilitative, maintenance, or personal care services" delivered outside an acute-care hospital for at least 12 consecutive months.

The critical distinction from standard health insurance lies in the type of care covered. Medicare does not cover custodial care — assistance with bathing, dressing, and eating — unless a qualifying medical need exists simultaneously. LTC insurance fills that gap.

How LTC Reinsurance Works

In LTC reinsurance, a primary insurer (the cedent) transfers a defined portion of its LTC policy reserves and associated liabilities to a reinsurer through a coinsurance arrangement. The reinsurer assumes a negotiated share of the block's liabilities and receives a corresponding share of assets. Recent transactions have used quota-share percentages ranging from 75% to 80%.

The cedent typically retains claim administration responsibilities while the reinsurer takes on investment management for the ceded assets.

Why LTC Is Uniquely Difficult to Reinsure

That structure sounds straightforward — the complexity lies in accurately pricing what gets transferred. According to RGA's analysis, LTC reinsurance demands expertise spanning actuarial modeling, claims forecasting, and investment management because it involves three intertwined risks simultaneously:

- Morbidity risk — incidence and severity of care claims

- Mortality risk — longevity of both claimants and non-claimants

- Claim duration risk — how long benefits are paid once triggered

Layer in illiquid, long-duration liabilities, and the pricing challenge is unlike most life or annuity blocks. Those compounding risks kept the reinsurance market largely dormant through much of the 2000s and 2010s.

The LTC Reinsurance Market Resurgence

Why the Market Was Dormant

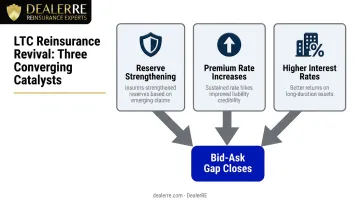

A persistent bid-ask spread — where buyers held more conservative views of LTC reserves than sellers, creating a valuation gap neither side was willing to cross. S&P Global characterized LTC reinsurance deals as "still a rarity" as recently as January 2025, noting that aside from Manulife's activity, very few new cessions had been identified.

Three catalysts converged around 2023 to close that gap:

- Primary insurers strengthened reserves in response to emerging claims experience

- Sustained premium rate increases made future liability projections more credible

- A higher interest-rate environment improved reinsurer return expectations on long-duration assets

The Three Landmark Transactions

Milliman's February 2026 analysis documents three standalone LTC coinsurance deals that collectively established a replicable transaction model:

| Transaction | LTC Reserves Ceded | Closed |

|---|---|---|

| Manulife / Global Atlantic | $4.4 billion | February 2024 |

| Manulife / RGA | $1.9 billion | January 2025 |

| Unum / Fortitude Re | $3.4 billion | July 2025 |

All three used coinsurance structures. All three bundled LTC with other liabilities — structured settlements, individual disability insurance — to improve overall transaction economics.

Broader Market Activity

Beyond the three headline deals, additional transactions confirm wide market engagement:

- Lincoln Financial / Fortitude Re — $28 billion in statutory reserves including MoneyGuard hybrid LTC (closed November 2023)

- RGA / MassMutual — approximately $1 billion in previously ceded LTC reserves recaptured (July 2023)

- Continental General / Munich Re — recapture of ~$350 million in Kanawha LTC policies (September 2025)

- Dreamscape / LifeSecure — ~$650 million in LTC reserves via entity acquisition (October 2025)

- Aquarian Capital / Brighthouse Financial — gross LTC reserves exceeding $5.8 billion (announced November 2025)

- Hildene / SILAC — ~$200 million net LTC reserves (December 2025)

The Role of Asset Managers and Private Equity

KKR backs Global Atlantic. Carlyle backs Fortitude Re. Both firms pursued LTC blocks primarily for the long-duration asset management opportunity — deploying capital into illiquid, higher-yielding investments matched against predictable long-term liabilities. To manage the actuarial risk they're less equipped to handle, both retroceded biometric risk entirely to rated global reinsurers.

This division — asset managers absorbing investment risk, rated reinsurers absorbing biometric risk — now defines how new entrants structure comparable transactions.

Key Factors Driving LTC Reinsurance Deals

Premium Rate Increases

For older policy blocks issued in the 1990s, a history of premium rate increases raises a specific concern: adverse selection. When healthy policyholders lapse after rate hikes while sicker ones retain coverage, the remaining block becomes progressively worse than original pricing assumed. This dynamic is most acute for policies with rich benefits like unlimited lifetime benefit periods, where policyholders have little economic incentive to lapse their coverage.

For newer policy vintages, the concern shifts. Cumulative rate increases have been lower, so buyers focus instead on whether future planned increases are likely to receive regulatory approval — and in what amounts.

Required Capital

Capital relief is often the primary motivation for cedents. LTC-heavy insurers can face capital overexposure, especially as blocks age and future premium run-rates decline, reducing the ability to offset adverse experience through further increases. Fitch estimated the Unum/Fortitude Re transaction would generate approximately $100 million in capital benefit for Unum.

Buyers and sellers frequently calculate required capital differently — using statutory rules, S&P rating frameworks, or internal actuarial models. That variation creates negotiating room. Critically, reinsurers with diversified product lines (particularly life insurance) face lower incremental capital requirements for LTC because mortality risk provides a natural hedge against LTC morbidity risk.

Investment Strategy

LTC liabilities are long-duration and illiquid. Claims may not commence for decades after policy issuance, and once triggered, can persist for years. Buyers' investment capabilities directly shape which block vintages they prefer:

- Older blocks — shorter remaining cash flows, matchable with shorter-duration assets

- Newer blocks — require longer-duration asset strategies, higher return requirements

Higher investment yields can help offset inflation in the cost of care, which remains a key risk driver for all LTC liabilities.

Block Characteristics and Deal Structures

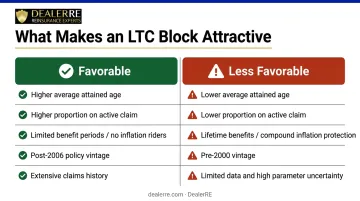

What Makes a Block Attractive

Not all LTC blocks are equally transactable. Milliman's analysis identifies the characteristics reinsurance buyers consistently prefer:

| Characteristic | Favorable | Less Favorable |

|---|---|---|

| Average attained age | Higher (more predictable near-term runoff) | Lower (greater forward uncertainty) |

| Proportion on active claim | Higher (known cost profile) | Lower (uncertain future incidence) |

| Benefit design | Limited benefit periods, no inflation riders | Lifetime benefits, compound inflation protection |

| Policy vintage | Post-2006 (tighter language, realistic pricing) | Pre-2000 (underpriced, generous terms) |

| Experience data | Extensive claims history | Limited data, high parameter uncertainty |

The Manulife/Global Atlantic block had an average attained age of 83 for active (non-claimant) lives. The subsequent Manulife/RGA deal involved a younger block averaging 75 — a meaningful shift toward blocks with more forward-looking uncertainty, demonstrating growing buyer confidence.

The Biometric Risk Retrocession Model

The structural approach that made this market viable is straightforward. In both the Global Atlantic and Fortitude Re transactions, the asset-manager-backed reinsurer retroceded 100% of biometric risk — morbidity and mortality — to a highly rated third-party global reinsurer. The PE-backed entity retained only spread-based investment risk.

This disaggregates LTC into two distinct challenges:

- Investment risk — suited to asset managers and PE firms

- Biometric risk — suited to rated specialist reinsurers

Without this structural split, the bid-ask spread would likely have remained prohibitive. Fitch confirmed this structure in both transactions, treating it as a credit-supportive feature for the cedents involved.

Deal Packaging

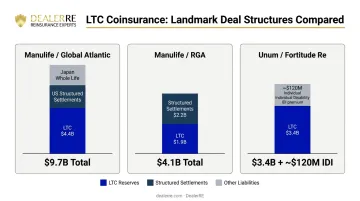

Bundling LTC with simpler liabilities has expanded the buyer pool by improving overall transaction economics. The pattern is consistent across all three major deals:

- Manulife / Global Atlantic: $4.4B LTC + US structured settlements + Japan whole life = $9.7B total

- Manulife / RGA: $1.9B LTC + $2.2B structured settlements = $4.1B total

- Unum / Fortitude Re: $3.4B LTC + ~$120M individual disability insurance in-force premium

The takeaway: packaging LTC alongside shorter-duration, more profitable liabilities isn't just deal mechanics — it's how sellers attract buyers and free up capital for higher-return businesses.

LTC Reinsurance Outlook: 2026 and Beyond

Milliman identifies 2026 and 2027 as key years for advancing momentum in LTC M&A and reinsurance transactions. Fitch's view is more measured, stopping short of expecting a "material number" of transactions in any single year, but both agree the established deal template will support continued selective activity.

Several trends point toward a broadening market:

- The Manulife/RGA deal's average insured age of 75 (vs. 83 in the first transaction) shows buyers are now comfortable underwriting younger, more forward-looking risk profiles

- Three outright company acquisitions in late 2025 point to entity-level buyouts emerging as a significant channel alongside traditional coinsurance structures

- Genworth and John Hancock alone held over $72 billion in gross LTC reserves at year-end 2023 — the $9.7 billion ceded through 2025 represents a fraction of what remains

The underlying logic driving this activity is consistent: structured reinsurance programs allow companies to retain more control over their risk profile, manage capital more efficiently, and improve long-term profitability. That principle isn't unique to the life and health insurance market.

Auto dealers applying a similar framework through dealer-owned reinsurance programs operate on the same foundation — retain the risk you understand, capture the underwriting profit you'd otherwise cede to a third party, and put that capital to work. DealerRE has helped dealerships apply this logic since 1994, supporting over 400 dealers nationwide in building self-insured F&I programs that keep underwriting profits inside the dealership.

Frequently Asked Questions

What is LTC insurance?

LTC (long-term care) insurance covers the cost of services when a person can no longer perform basic daily activities independently — such as nursing home care, assisted living, or in-home care. It differs from standard health insurance by covering custodial care, which Medicare does not cover unless a qualifying medical need exists.

What is the difference between LTC insurance and LTC reinsurance?

LTC insurance is sold directly to individuals to cover care costs. LTC reinsurance involves a primary insurer transferring a portion of those policy liabilities to a third-party reinsurer to manage capital, reduce risk concentration, and stabilize financial reserves.

Why are insurance companies looking to cede their LTC blocks?

Carriers cede LTC exposure to reduce capital overexposure, manage returns on required capital, and diversify their risk profile. For some, reserve activity also demonstrates liability adequacy to investors and regulators — serving both a financial and a regulatory signaling function.

What is biometric risk in LTC reinsurance?

Biometric risk refers to actuarial uncertainty tied to mortality (how long policyholders live) and morbidity (how likely they are to need care, and for how long). In recent LTC transactions, asset-manager-backed reinsurers have retroceded 100% of this risk to specialist global reinsurers, retaining only investment risk.

What makes an LTC block attractive to potential reinsurers?

Blocks with higher average attained ages, more lives already on active claim, limited benefit periods, no compound inflation riders, post-2006 underwriting vintages, and extensive historical claims data tend to generate the strongest buyer interest.

What is the outlook for LTC reinsurance activity in 2026 and 2027?

Milliman and Fitch both expect continued transaction activity, broader block vintages entering the market, and deeper participation from asset managers and established reinsurers. Both firms identify 2026–2027 as a period for building on the momentum established by the three landmark deals completed between 2024 and mid-2025.